Financial literacy matters because it helps you prevent making disastrous financial decisions, have adequate savings during retirement, avoids getting trapped in debt. It affects your life and your loved ones around you.

Benefits of financial literacy are tremendous

Here are 100 reasons: what is financial literacy and why is it important in Singapore

-

-

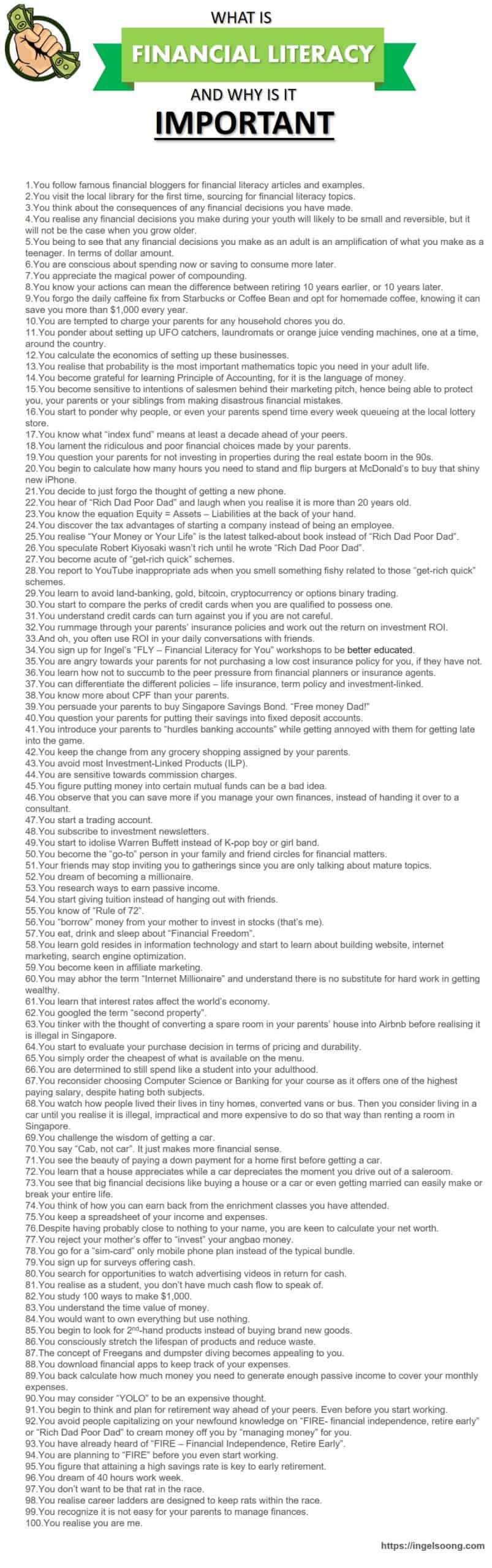

- You follow famous financial bloggers for financial literacy articles and examples.

- You visit the local library for the first time, sourcing for financial literacy topics.

- You think about the consequences of any financial decisions you have made.

- You realise any financial decisions you make during your youth will likely to be small and reversible, but it will not be the case when you grow older.

- You being to see that any financial decisions you make as an adult is an amplification of what you make as a teenager. In terms of dollar amount.

- You are conscious about spending now or saving to consume more later.

- You appreciate the magical power of compounding.

- You know your actions can mean the difference between retiring 10 years earlier, or 10 years later.

- You forgo the daily caffeine fix from Starbucks or Coffee Bean and opt for homemade coffee, knowing it can save you more than $1,000 every year.

- You are tempted to charge your parents for any household chores you do.

- You ponder about setting up UFO catchers, laundromats or orange juice vending machines, one at a time, around the country.

- You calculate the economics of setting up these businesses.

- You realise that probability is the most important mathematics topic you need in your adult life.

- You become grateful for learning Principle of Accounting, for it is the language of money.

- You become sensitive to intentions of salesmen behind their marketing pitch, hence being able to protect you, your parents or your siblings from making disastrous financial mistakes.

- You start to ponder why people, or even your parents spend time every week queueing at the local lottery store.

- You know what “index fund” means at least a decade ahead of your peers.

- You lament the ridiculous and poor financial choices made by your parents.

- You question your parents for not investing in properties during the real estate boom in the 90s.

- You begin to calculate how many hours you need to stand and flip burgers at McDonald’s to buy that shiny new iPhone.

- You decide to just forgo the thought of getting a new phone.

- You hear of “Rich Dad Poor Dad” and laugh when you realise it is more than 20 years old.

- You know the equation Equity = Assets – Liabilities at the back of your hand.

- You discover the tax advantages of starting a company instead of being an employee.

- You realise “Your Money or Your Life” is the latest talked-about book instead of “Rich Dad Poor Dad”.

- You speculate Robert Kiyosaki wasn’t rich until he wrote “Rich Dad Poor Dad”.

- You become acute of “get-rich quick” schemes.

- You report to YouTube inappropriate ads when you smell something fishy related to those “get-rich quick” schemes.

- You learn to avoid land-banking, gold, bitcoin, cryptocurrency or options binary trading.

- You start to compare the perks of credit cards when you are qualified to possess one.

- You understand credit cards can turn against you if you are not careful.

- You rummage through your parents’ insurance policies and work out the return on investment ROI.

- And oh, you often use ROI in your daily conversations with friends.

- You sign up for Ingel’s “FLY – Financial Literacy for You” workshops to be better educated.

- You are angry towards your parents for not purchasing a low cost insurance policy for you, if they have not.

- You learn how not to succumb to the peer pressure from financial planners or insurance agents.

- You can differentiate the different policies – life insurance, term policy and investment-linked.

- You know more about CPF than your parents.

- You persuade your parents to buy Singapore Savings Bond. “Free money Dad!”

- You question your parents for putting their savings into fixed deposit accounts.

- You introduce your parents to “hurdles banking accounts” while getting annoyed with them for getting late into the game.

- You keep the change from any grocery shopping assigned by your parents.

- You avoid most Investment-Linked Products (ILP).

- You are sensitive towards commission charges.

- You figure putting money into certain mutual funds can be a bad idea.

- You observe that you can save more if you manage your own finances, instead of handing it over to a consultant.

- You start a trading account.

- You subscribe to investment newsletters.

- You start to idolise Warren Buffett instead of K-pop boy or girl band.

- You become the “go-to” person in your family and friend circles for financial matters.

- Your friends may stop inviting you to gatherings since you are only talking about mature topics.

- You dream of becoming a millionaire.

- You research ways to earn passive income.

- You start giving tuition instead of hanging out with friends.

- You know of “Rule of 72”.

- You “borrow” money from your mother to invest in stocks (that’s me).

- You eat, drink and sleep about “Financial Freedom”.

- You learn gold resides in information technology and start to learn about building website, internet marketing, search engine optimization.

- You become keen in affiliate marketing.

- You may abhor the term “Internet Millionaire” and understand there is no substitute for hard work in getting wealthy.

- You learn that interest rates affect the world’s economy.

- You googled the term “second property”.

- You tinker with the thought of converting a spare room in your parents’ house into Airbnb before realising it is illegal in Singapore.

- You start to evaluate your purchase decision in terms of pricing and durability.

- You simply order the cheapest of what is available on the menu.

- You are determined to still spend like a student into your adulthood.

- You reconsider choosing Computer Science or Banking for your course as it offers one of the highest paying salary, despite hating both subjects.

- You watch how people lived their lives in tiny homes, converted vans or bus. Then you consider living in a car until you realise it is illegal, impractical and more expensive to do so that way than renting a room in Singapore.

- You challenge the wisdom of getting a car.

- You say “Cab, not car”. It just makes more financial sense.

- You see the beauty of paying a down payment for a home first before getting a car.

- You learn that a house appreciates while a car depreciates the moment you drive out of a saleroom.

- You see that big financial decisions like buying a house or a car or even getting married can easily make or break your entire life.

- You think of how you can earn back from the enrichment classes you have attended.

- You keep a spreadsheet of your income and expenses.

- Despite having probably close to nothing to your name, you are keen to calculate your net worth.

- You reject your mother’s offer to “invest” your angbao money.

- You go for a “sim-card” only mobile phone plan instead of the typical bundle.

- You sign up for surveys offering cash.

- You search for opportunities to watch advertising videos in return for cash.

- You realise as a student, you don’t have much cash flow to speak of.

- You study 100 ways to make $1,000.

- You understand the time value of money.

- You would want to own everything but use nothing.

- You begin to look for 2nd-hand products instead of buying brand new goods.

- You consciously stretch the lifespan of products and reduce waste.

- The concept of Freegans and dumpster diving becomes appealing to you.

- You download financial apps to keep track of your expenses.

- You back calculate how much money you need to generate enough passive income to cover your monthly expenses.

- You may consider “YOLO” to be an expensive thought.

- You begin to think and plan for retirement way ahead of your peers. Even before you start working.

- You avoid people capitalizing on your newfound knowledge on “FIRE- financial independence, retire early” or “Rich Dad Poor Dad” to cream money off you by “managing money” for you.

- You have already heard of “FIRE – Financial Independence, Retire Early”.

- You are planning to “FIRE” before you even start working.

- You figure that attaining a high savings rate is key to early retirement.

- You dream of 40 hours work week.

- You don’t want to be that rat in the race.

- You realise career ladders are designed to keep rats within the race.

- You recognize it is not easy for your parents to manage finances.

- You realise you are me.

-